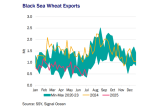

In the year-to-date, Black Sea wheat exports have been 46% lower than the same period last year, according to vessel tracking data. The hot and dry weather in Europe has raised further concerns about upcoming exports.

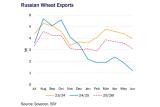

In the first half of this year, Russian wheat exports had been kept artificially low due to the country limiting exports to 11 Mt from mid-Feb to the end of June. This contributed to 1h25 shipments being less than half that of the same period in 2024.

Due to last season’s restrictions, at 42.9 Mt, Sovecon’s most recent export forecast for 25/26 (Jun/Jul) comes in 3.8 Mt above the estimated exports for 24/25. Though the next season’s exports are expected to be 9.1 Mt below the strong 23/24 season.

If we apply the forecasted 42.9 Mt over the next year to Russia’s typical export seasonality, excluding 24/25 where exports were hampered by restrictions, it implies a weaker start to the upcoming months. This is important for vessel demand, lessening support for Panamax and geared vessels out of the Black Sea in Q3 and Q4.

One near-term positive is that Russia’s export tax has fallen to zero for the first time since its introduction in 2021, potentially prompting farmers to sell amid a slow start to the season. The export tax was implemented to protect the domestic market from higher prices. Although, the weak international price environment and lower ending stocks (-14% y-o-y) may hamper this export push.

Ukraine, meanwhile, offers limited support for Black Sea exports. In the first half of the year, wheat exports were 4.7 Mt lower year-on-year at 5.5 Mt. Ukraine’s challenging export environment has not been limited to wheat, with a decline seen also in Ukrainian volumes of barley (-1.1 Mt to 0.3 Mt) and corn (-7.6 Mt to 11.6 Mt), according to Ukrainian Agriculture Ministry data. Conversely, soybean exports have recorded a 0.6 Mt increase to 1.8 Mt.

With production and export infrastructure difficulties since the start of the invasion of Ukraine, profitability has been an ongoing issue. The area harvested has dropped dramatically for grains, with barley (-40%), corn (-25%) and wheat (-30%) all hit hard since the start of the war, USDA data show. Though exports of the aforementioned grains have declined since the war began, it is worth mentioning that due to lower domestic consumption, Ukraine has been able to export a larger share of its production.

While still remaining a small global player for soybean exports at 3.8 Mt in 24/25, the country has doubled its harvest area since before the war (in the 21/22 season) and increased exports by 2.4 Mt.

Attempting to maximise the logistical benefits of its location, Ukraine has increased its market share of wheat exports to North Africa (+1.8 Mt y-o-y to 5.1 Mt), competing with Russian and EU supplies. However, amid lower total exports, longer-haul trade to Asia has fallen (- 0.8 Mt to 5.5 Mt).

The EU has reintroduced quotas on Ukrainian agriculture after two years, which may increase Ukraine’s market share in North Africa and further afield. The wheat import quota has been set at 1.3 Mt, Reuters reports, representing a 70% decline from the 4.9 Mt in the 24/25 season. This may result in a marginal seaborne tonne-mile benefit, as overland cargoes had increased to the EU as a result of the war. However, Ukrainian wheat railings already fell 1.0 Mt y-o-y to 0.4 Mt in the 24/25 season, according to Ukrainian Agriculture Ministry data, well under the quota. Furthermore, increased Ukrainian supplies to other destinations will likely be countered by a reduction in EU exports, as it diverts more to its domestic market following the introduction of quotas.

By Cara Hatton, Dry Bulk Analyst, Research, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business