International trade policy has been a wild ride since the so-called “Liberation Day” touted by US President Donald Trump. Threats, escalation followed by de-escalation, pauses and constant changes have riddled the industry, creating massive uncertainty and volatility in US trade with the rest of the world. And despite some claims to the contrary, it is already becoming more and more apparent that all this is having a tangible impact on trade flows.

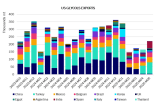

US Glycols Exports

Trade is like water – it always finds a way to flow around any obstacles. In the process the flow changes its direction and its path but continues. And where used to flow a river, after this change there may be just a trickle. Metaphors aside, in the chemicals trade we are witnessing something similar happening in real time. Cargo flows are being reshuffled as a result of the obstacles created by the US.

It was already apparent in the days immediately after Liberation Day when almost overnight spot enquiries for cargoes from US Gulf to China dried up and it became eerily quiet.

The US, one of the largest glycols exporters in the world with 3.3 million mt in 2024 has been relying on China to absorb about 30% of this quantity. It’s been a steady, reliable cargo flow, providing employment for the chemical tankers on the Transpacific Lane. The average monthly export quantity to China for 2024 was around 85,000 mt.

From early this year, though, China appears to have embarked on a strategy of diversification and has been reducing glycols imports from the US. From April onwards though when the tariff spat escalated, the US has exported close to zero glycols to China. (The current tariffs applied to US imports into China stand at 15%, while the US applies 30% on products from China).

With a million mt of glycols having to find a new home, US producers have been trying hard to find new destinations for their product, but this has been an uphill battle. Traditional buyers such as Turkey, Mexico, Belgium or Brazil lack the market depth to absorb this volume. And India – the only other country with the ability to take this extra quantity is conveniently located near the Middle East which is the largest glycols-producing region in the world. As a result of this, the US market remains oversupplied with glycols, prices are depressed, and some plants are running at lower rates or are shut.

The Impact on Shipping

The plight of US glycols producers has spilled over to the shipowners whose chemical tankers call the US Gulf. Considering the exported volumes and their destinations, one can easily calculate the tonne-miles generated by the US glycols exports – and it doesn’t look pretty.

The overall loss of exported volume has meant the tonne-miles demand from glycols exports has roughly halved. As a result of this, freight rates out of the US Gulf to the Far East have been steadily dropping since April.

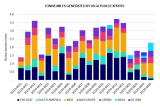

The glycols volumes from the US have been partially substituted with im-ports into China from other sources such as Canada or Taiwan. The latter exported to China 235,000 mt in the first 5 months of this year — more than double the volume from all of 2024.

However, there appears to be some degree of demand destruction for imported glycols in China due to slower downstream demand from end consumers in the domestic Chinese and overseas markets.

The Fleet Used for US Glycols Exports

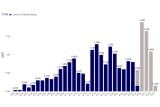

Glycols require stainless steel or marineline chemical tankers and are usually exported from the US in lots of 20-40,000t to long-haul destinations in Asia, India or Europe. The current size of the segment, suitable to carry glycols from the US, is 509 ships. The average age of these ships is around 11.5 years, which means they still have at least another 10 years of work life till they are sent for recycling. However, the orderbook comprises 158 ships, or almost 34% of the existing fleet with a spike in deliveries expected in 2026 and 2027.

Even considering the potential scrapping of the older tonnage, the projected growth in this segment is going to be strong, especially in 2026 and 2027 (7.0% and 4.4% respectively) and this, coupled with the lower tonne-miles demand from the US, does not bode well for the ship earnings in this segment – unless the world has enough of tariffs.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business