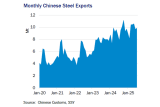

For the minor bulk trades, one of the positive surprises of the year has been the continued growth in Chinese steel exports. Based on official customs data, exports in the first seven months of 2025 totaled 68Mt (up 8.9% y-o-y) — a new record high for the calendar period (if only marginally higher than the 67.6Mt seen in 2016).

The continued ability of the Chinese export machine to adapt to higher global trade barriers is perhaps surprising. One possible explanation is the frontloading of export volumes before the global trade situation gets worse. However, it is also clear that the implementation of tariffs, import quotas and other anti-dumping measures does not address the root cause of the problem: overcapacity in global steel production. While import barriers may protect a high-cost domestic steel industry in the name of local employment and national security in the short run, its introduction does not improve the competitiveness of a country’s producers in the global export market. On the contrary, protected industries may be increasingly unable to compete in the international market, leaving more room for the most cost-efficient (or subsidised) operators, such as Chinese steel mills.

There are also plenty of workarounds to bypass tariffs on Chinese steel. Notably, semi-finished products such as steel billets are often exempt, and have seen a large jump in export volumes accordingly. It is also clear, though much harder to quantify empirically, that Chinese exports of steel as a part of finished goods, such as electric cars, white goods, and even newbuild ships, are a lot higher now than was the case during the last steel export boom a decade ago. These sources of export demand are a lot harder to cut off politically and so provide an alternative outlet for Chinese steel exports.

What, then, about the overall health of the Chinese steel industry at the moment? In short, it seems better than has been the case for some time, even in the absence of stimulus packages for the “old” steel–intensive industries and the property market.

According to official numbers, Chinese crude steel production in the first half of the year was down 3.0% to 515Mt, while pig iron production held up a bit better, down 0.8% to 434Mt. However, survey-based data from Mysteel suggests that the average daily iron output in the first seven months of the year was up 3.2% y-o-y, with output now near the highs seen back in October 2023 (ref. above chart). An important indicator of the health of the industry is obviously profitability. The good news is that the percentage of profitable Chinese steel mills has been kept unusually stable and relatively high thus far in 2025. Survey-based data suggests that more than 68% of steel mills were profitable on a cash cost basis per August 8, up from a mere 6.5% a year ago. August 2024 was also the month when Chinese steel industry leaders famously warned of a “long and harsh winter” over weak demand and overcapacity, only for optimism to quickly return a month later when China’s central bank unveiled a comprehensive stimulus package to prevent a further economic slowdown, the positive effects of which have seemingly lasted until now.

So, despite continued “doom and gloom” in some of the macro headlines regarding China, notably about price deflation, oversupply in many industry sectors, a still-deflating property bubble, and the effects of trade wars, the sentiment and outlook for China’s steel industry — all important for the global dry bulk freight market — is actually pretty good. The key, as usual, is competitiveness and while politicians can argue over unfair trade practices and attempt to put up trade barriers, the cheapest supplier in a commoditised market always wins in the end.

By Roar Adland, Senior Director & Global Head of Research, SSY

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business