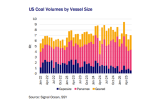

Coal’s growing role as the ‘equalizer’ or perhaps ‘shock absorber’ of the dry bulk freight market is becoming increasingly evident, as the global coal trades adapt to the fleet imbalances created by the strong demand from the iron ore and bauxite trades. As the Capesize segment becomes increasingly dominated by long-haul iron ore and bauxite trades — especially out of the Atlantic — coal has become the trade where redistribution of cargo across vessel segments is most visible. With more Capesize tonnage tied up elsewhere, a tightening supply of available ships in the Pacific has eroded Capesizes’ coal market share, shifting cargoes toward the smaller vessel classes, most notably Panamaxes. What is new is that much of this shift is a result of fleet allocation and availability challenges, and not a pure cost-based decision, as Capesize rates still rarely exceed Panamax voyage rates due to economies of scale.

SSY predicted this shift in our Dry Bulk Forecaster report last year, pinpointing Australian coal as the likely pivot point. The data so far in 1H25 confirms this, as Capesize Australian coal liftings dropped to just 62.3 Mt — its lowest in at least a decade — while Panamax volumes climbed to a record 95.4 Mt. The loss in market share has been most evident at the Port of Newcastle, where 1H25 Capesize volumes fell by 7.6 Mt year-on-year, partly offset by a 3.8 Mt gain for Panamaxes. Smaller shifts have also been recorded at Abbot Point and Hay Point (Capesize: -3.9 Mt; Panamax: +0.9 Mt).

To put this in perspective, the Australian market typically sees around 90 Capesize coal cargoes per month in the first half of the year. This year, however, the average has dropped to 73, with February sinking to just 54 cargoes— the lowest in recent history. It’s important to note that while some of that loss has been caused by the shift to Panamaxes, part of it also reflects weakening underlying coal demand this year.

What’s perhaps more telling is the absence of a corresponding pickup in the geared segment. Contrary to expectations, this rebalancing has not trickled down further. In fact, smaller ships are also carrying less coal, leaving Panamaxes as the only size class seeing real growth in the coal trade. The fact that this growth is happening despite lower total coal trade makes the shift between sizes even more noticeable.

Australia isn’t alone. Coal trades from the United States and South Africa are undergoing similar structural changes. In South Africa, thanks to robust Indian demand in the pre-monsoon period and improved Transnet operations, 1H25 exports rose 4.7% year-on[1]year. But even here, Capesize volumes are shrinking as more and more stems are being marketed for the Panamax segment. On the key Richards Bay–India route, 1H25 Capesize volumes fell 0.7 Mt, while Panamaxes added 3.7 Mt, translating to 25 additional cargoes.

In the US, Capesize volumes never fully recovered after the collapse of the Francis Scott Key bridge in Baltimore. Despite a very strong 2024 coal export season in the US, Cape volumes saw little growth. In the first half of this year there have been very few Capesize coal cargoes marketed, with only 33 Capesize stems in 1H25, compared to 40 cargoes seen just in the first quarter last year. It was only a few years ago that the Panamax share of US coal loadings hovered around 40-45%, playing a comparable role to the Capesize share of 30-35%. However, since then, Panamaxes have quietly filled the gap, and in the first half of the year, the Panamax share of US coal trade has surpassed 60%, while the Capesize share has dropped to just 10%, highlighting the shift toward smaller, more readily available vessels.

Altogether, these changes highlight the self-regulating ability of the dry bulk market to adapt to imbalances between segments. Coal, often seen as a steady and mature market, is now playing an important role in reshaping the market balance between ship sizes.

By Hamid Agassi, Dry Bulk Analyst, Research, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business