Posts

21/12/23

LNG Update: Diversions of a handful of LNG carriers due to escalating tensions in the Red Sea, market impact at present remains minor

Recent attacks by Houthi militants on ships in the Red Sea have prompted the diversion of at least 5 LNG carriers away from the Suez Canal and towards the Cape of Good Hope since last Friday, according to Kpler.

In response to the heightened security situation, several Owners and Charterers have confirmed that they have paused transiting the Suez Canal, including BP and COSCO Shipping, among others. However, the situation is still evolving, and we may see more Owners and Charterers avoiding the canal.

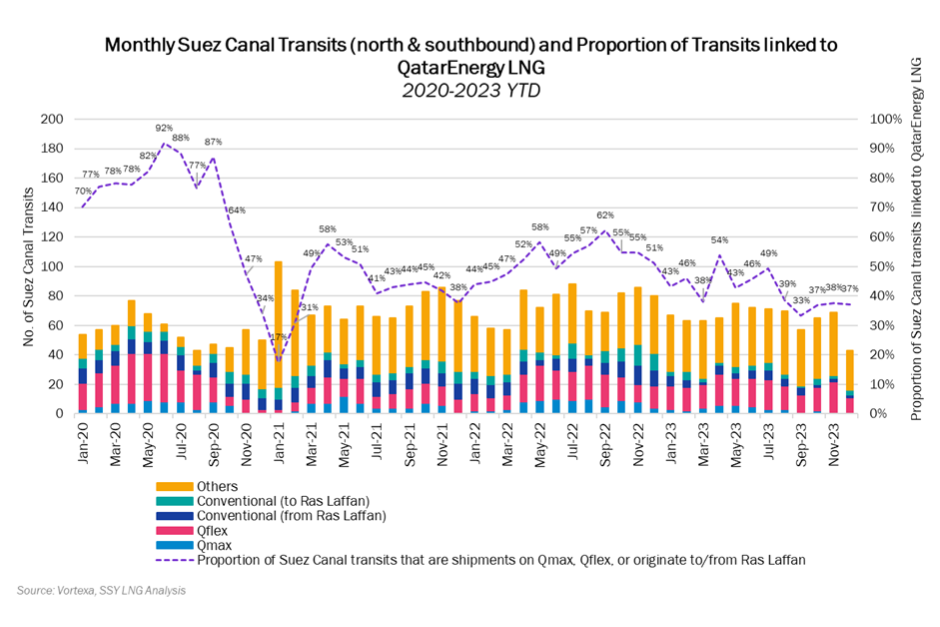

According to data from Vortexa, there are, on average, 67 Suez Canal transits by LNG tankers per month (north and southbound since 2020). Approximately 53% of these transits are linked to QatarEnergy LNG and only 22% of the transits originate from or are destined for the US Gulf Coast. Given its reliance on the Suez Canal, if the security situation continues to escalate, QatarEnergy LNG could be the most affected; the number of voyage days from Qatar to Northwest Europe would almost double, increasing from around 14-16 days via the Suez Canal to around 26-28 days via the Cape of Good Hope (assuming a speed of 17 knots). This would have a significant impact on shipping demand, increasing the number of vessels required per year from around 18-19 to 33-34, according to SSY LNG’s calculations (this is based on LNG flows from Qatar to Europe from January to November this year and extrapolated for the whole of 2023). However, some sources are of the view that given Qatar’s relationship with neighboring countries, it is unlikely that QatarEnergy LNG will reroute their vessels away from the Suez Canal to the Cape of Good Hope unless the Headowners of these vessels refuse to transit.

It is also worth highlighting that the number of voyage days from the US Gulf Coast to Asia via the Suez Canal or the Cape of Good Hope is similar, increasing by approximately 3 days for voyages using the Cape. As such, the impact on shipping demand is minimal with the number of additional LNG vessels required per year increasing by 1-2, according to SSY LNG’s calculations (this is based on LNG flows from the US to Asia from January to November this year and extrapolated for the whole of 2023).

We currently expect the ongoing situation in the Suez to lend some support on spot rates in the second half of January and the first half of February, with some players short covering vessels previously scheduled to load in the US Gulf after transiting the Suez in their previous voyage and others simply seeking to capitalise on the market’s uncertainty. Yet, this “squeeze” might be short-lived since the market remains quite backwardated as we exit the winter months and move into the 2HQ1-Q3 period when the market has historically been long. Importantly, rates will also depend on the persistence of the current cold snap in the East which is seeing parts of South Korea, Japan and China experience freezing temperatures.

The global shipping community is monitoring the Suez Canal closely and trying to anticipate which Owners, Charterers and operators will follow the cautious route around the Cape, or brave the transit once more. Any escalation of the situation will lend support in the front months (January and February), but the pressure of a fundamentally backwardated market moving into the Spring is not expected to be challenged.

By Kyla Schliebs, Head of LNG Research, Philip Tripodakis, Partner, LNG & Scott Leong, General Manager, LNG.

Articles

You may also be

interested in

View all

{kind=link}

Get in touch

Contact us today to find out how our expert team can support your business