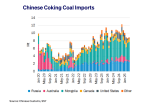

The decline in Chinese coal imports has been a focal point recently. The decrease has largely been driven by thermal coal (down 6% to 116.3 Mt in Jan—Apr, incl. lignite) while coking coal has remained more resilient, declining 3% to 36.4 Mt.

However, of even greater importance for vessel demand, within the decline in coking coal imports we have seen an 18% drop in overland cargoes from Mongolia to 15.7 Mt. If we exclude cargoes from Mongolia, Chinese coking coal imports have actually risen 12% to 20.7 Mt.

Mongolian coking coal recorded dramatic growth from 2022 to 2023, more than doubling from 25.6 Mt to 53.9 Mt over the year. The country maintained this level into 2024 at 56.8 Mt and accounted for 47% of China’s total coking coal imports. More recently, concerns have been mounting over the prospect of Mongolian coal cargoes facing export disruptions, as the country’s prime minister stepped down earlier this month and political pressure builds over profiteering off of the country’s mineral resources.

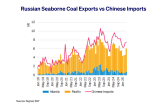

In order to assess the impact of these changes on the seaborne market we also have to consider Russian coking coal exports to China, which have held a market share above 25% for the past three years. China’s total (thermal and coking) coal imports from Russia rose 0.5 Mt year-on-year in the year-to-April according to customs data; however, vessel tracking data show a 1.8 Mt decline across the same period. While these data sources are not exactly comparable, the widening gap over the previous few years suggests a greater share of overland cargoes.

Furthermore, the tonne-mile gain from China switching from Mongolian cargoes to seaborne Russian cargoes is undermined by the greater share of volumes coming from Russia’s Pacific ports. The share of Russia-China coal shipments from Atlantic ports peaked at 20% of the total in 2023 but has since fallen to 9% in Jan-May this year. Russia is further upgrading its Pacific ports, with McCloskey reporting the Daltransugol terminal at the Port of Vanimo has completed a project to lift its coal export capacity 9 Mt to nearly 33 Mtpa, enabled by improved rail connections.

This increase in overland and short-haul shipments to China comes while Russia’s total coal exports have been declining after reaching 233.0 Mt in 2021 and falling to 187.3 Mt in 2024. Overall, any potential further disruption to Mongolian coal exports should have a marginal positive impact on seaborne tonne-mile demand, as the country has such a large market share in the Chinese market. Russian volumes could benefit; however, Russian coking coal production has already been in decline from lower coal prices and export infrastructure restrictions, so their ability to quickly meet gaps in demand may be limited.

It is also important to note the potential headwinds for Chinese steel demand in the coming months. Amid lower Mongolia-China coal exports, stocks have been building at the Mongolia border as the effects of weaker demand from China have kicked in. McCloskey report stocks in Ganqimaodu rose from below 3.5 Mt in early May to above 4.0 Mt the same period in June.

There are also expectations of weaker steel production in China, despite a broadly positive start to the year, as China’s National Development and Reform Committee has announced a 50 Mt reduction in steel capacity by the end of the year. The actual implementation may not lead to a 50 Mt cut, though any reduction will help to limit the country’s booming steel exports that are pressuring domestic steel production in other Asian nations. Any rebound in other Asian steel producing nations locations will potentially diversify coking coal shipments away from China – and importantly away from overland Mongolian and Russian cargoes.

By Cara Hatton, Dry Bulk Analyst, Research, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business