After rallying on the back of supply chain disruptions and subsequent scarcity in 2021 and 2022, coal prices have dropped considerably. Australian semi-soft coking coal FOB prices have declined from an average $269/t in 2022 to $150/t in 2024, further easing to $130/t in the year-to-date.

The lower price environment has been brought about by a number of dark clouds on the economic horizon. Increased tariffs and trade barriers bring into question global growth and steel demand in general, while the potential for reduced Chinese steel exports later this year threatens demand from the largest steel producer. Looking further ahead, though, the well-known cyclical nature of commodity markets raises questions about whether coking coal markets will tighten up again.

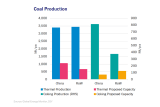

Australia is the largest coking coal exporter, shipping 152.9 Mt last year, ABS data show, with the vast majority of its coking coal supplies exported. This marks a stark decline from the peak of 188.1 Mt in 2016. In addition to subdued coal prices, the country faces increasing operational costs. High labour costs come amid raised royalty costs, at a time when the financing of fossil fuel projects is being restricted as environmental, social, and governance (ESG) goals grow in prominence. Australia’s Resources and Energy Quarterly report states that coal exploration spending fell 32% q-o-q in 1q25.

Russia, meanwhile, faces its own distinct problems. The country has fewer markets to export to due to sanctions, pressuring prices, all the while facing a stronger RUB to USD exchange rate and higher logistical costs, resulting in mines struggling to remain profitable at prevailing export prices. Persistently high interest rates (18%) also make financing expensive. The country’s government is propping up exports through support of rail use and taxation deferrals – prompting the question of how long miners and the government can delay closures.

All these issues predate the uncertainty caused by the prospects of secondary tariffs by the US Administration. While China is unlikely to be influenced by their implementation, India and Southeast Asian markets could move towards lessening trade with Russia. China imported 14.8 Mt of coking coal from Russia in the first half of the year, while India and Vietnam imported 8.3 Mt and 0.5 Mt, respectively. Turkey also remains a major importer of Russian coal, having imported 0.3 Mt in 1h25, and may be encouraged to import increased amounts from US suppliers – of which it already imported 1.0 Mt from in 1h.

In the US, the well-publicised goal to attract manufacturing onshore and, specifically, strengthen the domestic steel industry would result in more coal being used domestically. US coking coal production declined 7.4% y-o-y to 15.9 Mt, McCloskey data show, on the back of further coking coal mine closures.

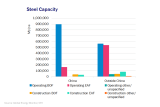

Of course, any future tightness in coking coal supply will depend on steel demand and the pace of the green transition. Global Energy Monitor data show that 55% (35.1 Mtpa) of the steel capacity under construction in China is BOF, adding to the 1,055.8 Mtpa already operational. Elsewhere, EAF production is taking on greater prominence, with 34% (44.0 Mtpa) being BOF capacity. At the other end of the spectrum, 72% (28.9Mtpa) of India’s capacity under construction is BOF.

Coking coal prices have found some support recently from the announcement of China’s mega-dam construction in Tibet, with reports of up to 6Mt of steel demand from the project. Crackdowns on coal overcapacity in the country have also propped up prices, though it is worth remembering similar attempts to cut overcapacity in steel appear less successful in a competitive market. Meanwhile, India has the goal to reach 300 Mt of steel capacity by 2030. Last year India produced 149.4 Mt of steel, requiring 75.1 Mt of coking coal imports.

By Cara Hatton, Dry Bulk Analyst, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business