The rainy season has well and truly started in Guinea and can be expected to bring with it the typical seasonal weakness in bauxite exports, but usual seasonal patterns aren’t the only concerns for the seaborne bauxite market as the Guinean government ramps up attempts to stamp its authority on the mining and export process.

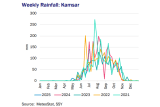

But first, the weather. Thanks to the West African Monsoon, Guinea has a pronounced rainy season from the start of May to the end of October. Almost no rain falls in the country between the start of December and the end of April, but then picks up throughout May peaking around mid August. Rainfall in Kamsar, the main port for Bauxite exports, peaks at around 150 mm per week most years (compared to a around 60mm over a month in the wettest time of the year in London). Between 2nd and 9th July just over 70 mm of rain fell in Kamsar, a particularly wet week for this time of year.

When the rain picks up, exports tend to suffer – for the last 7 years exports over May to October have been lower than the previous six months as the rain disrupts mining, internal logistics and port/transshipment operations. The chart to the right compares weekly exports on the x-axis with weekly rainfall on the y-axis during the monsoon season for each of the past 5 years. Each year shows a negative correlation as weeks with heavier rainfall tend to be the weeks with weaker exports.

The chart also shows, however, the very strong growth in exports generally. Every year Guinea is exporting more bauxite even during the weeks with heavy rainfall. In fact, even though 2024 saw a particularly wet monsoon season, with average daily rainfall of 11.7 mm, up 31.4% y-o-y, exports were only marginally below the preceding six months (-0.2%). 2025 has offered no exception to the period of strong growth, with exports in the first six months of the year up 32% y-o-y, including a 46% y-o-y climb in May exports and a 16% y-o-y climb in June. In fact exports in June hit 15.1 Mt according to vessel tracking data, higher than any month of 2024, despite rainfall levels already beginning to pick up.

So whilst we can expect exports to drop over the next few weeks going into August (usually the rainiest month), continuing underlying growth may be expected to offset seasonal weakness to some extent. On the other hand, interference from Guinea’s military junta poses a less predictable and potentially more serious risk.

The first signs of the government’s intention to increase their influence on bauxite operations in the country came in October last year when they suspended the export licence of EGA. In May Guinea made steps to completely revoke EGAs licence over concerns that the Emirati company hadn’t invested enough to keep some of the aluminium value chain within the country. More recently the Minister of Mines and Geology announced plans to introduce a Guinea Bauxite Index (GBX) at the end of 2025 as a national pricing benchmark ostensibly to reduce transfer pricing (whereby bauxite is sold between separate entities of a multinational in order to maximise profits in the lowest taxed jurisdiction). At the same time policy was announced for 50% of all Guinean bauxite to be shipped on Guinean flagged vessels, and for the introduction of a Guinean national shipping company to take responsibility for shipping bauxite, and the government also announced intentions to enforce the right they officially have to market 15% of the production of each mining company.

Guinea is the largest producer of bauxite in the world and political disruption is unlikely to change that in the mid term. However, increased interference makes Guinean bauxite less attractive and could signal the end to the exorbitant growth seen over the past few years.

By William Tooth, Senior Dry Bulk Analyst, Research, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business