Since the start of 2026 coal prices have been creeping higher across all major exporters. News of a Sumatran trucking ban and whispers of tighter domestic coal policy in China nudged markets higher, but the headline grabber is Indonesia’s proposal for steep supply cuts and a new export duty. Guidance from Jakarta remains ambiguous, with the cuts described as “incomplete”. Though this can look like political backtracking as Indonesia has done many times before, it is worth considering who would benefit if the measures do stick.

South Africa and Mozambique are among the best positioned to capture any displaced volumes into India. South African exports are regaining momentum as Transnet’s rail network stabilises, with improved security and better train performance lifting near‑term capacity. In the longer term, one of the main issues — shortage of rail wagons — will be easing as third‑party rolling stock enters the system from 2H26. There was also a government inquiry into private partnerships to upgrade Transnet’s rail and port assets, which attracted numerous submissions; project bids are expected soon.

After a multi-decade low of 47.2 Mt in 2023, rail performance has slowly improved and rail flows to RBCT recovered to 56.8 Mt in 2025 (all-time peak: 76 Mt). With recent rail ops improvements, RBCT’s target for this year has been set at 65 Mt, an 8 Mt growth. Transnet’s five-year plan to lift rail capacity toward roughly 77 Mtpa should support RBCT volumes beyond this year.

Truck shipments via alternative routes expanded in the years that rail was struggling. Non-RBCT volumes peaked at 25 Mt in 2023, redirected to terminals in Maputo, Matola and Durban as exports bypassed the rail corridor. But trucking is costly and becomes uneconomical below $100 per tonne, so those diverted volumes have been falling as coal prices softened the past few years.

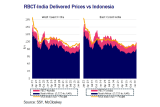

India remains by far the biggest buyer of South African coal, but demand last year was patchy. 2025 started off strong but rupee weakness and volatile pricing pushed some buyers to the sidelines in 2H25. Nevertheless, total South African coal exports rose 0.9 Mt year-on-year to reach 71.9 Mt in 2025. Though RBCT volumes were up by 5.6 Mt, coal volumes from elsewhere fell as trucking becomes more uneconomical.

Longer term, India will drive most of the seaborne coal import growth this decade. Despite its rapid GDP growth, India still faces severe energy poverty. Where a developed country like the US uses around 76,800kwh of electricity per person, in India this figure is only at 7,800kwh/person. Being the world’s most populous country, even small gains in per-capita consumption can translate into large swings in seaborne coal demand. Beyond power generation, higher quality South African coal has been very popular with Indian sponge iron and cement industries, which are mostly situated on the west coast. Indian sponge iron output is expected to grow by ~20 Mtpa by 2030 and with 1.2 of coal for each tonne of sponge iron, this would likely create more demand than South Africa can meet by itself.

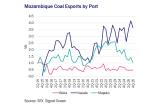

Mozambique will also compete for some of that demand, backed by some the world’s largest untapped coal reserves. It exported 21.6 Mt in 2025, mainly from Nacala, which has grown for five consecutive years to 14.0 Mt (+0.8 Mt yoy). While South African re‑exports through Maputo have halved over the past few years with weaker prices, Mozambique’s own flows are rising supported by expansion projects. There are three significant expansion projects today: TCM Maputo expansion from 7.5 to 12 Mtpa in 2027, a new 25 Mtpa port in Macuse and expansion of the current Sena and Nacala corridors. Further, under government’s Economic and Social Plan, there are plans to add over 750 wagons in the short term and a longer-term plan of further 250 wagons and 15 locomotives by 2030, all of which could significantly expand coal capacity and exports.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business