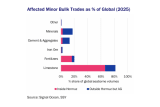

While the energy impact of the Middle East Gulf (MEG) war naturally catches most of the headlines, the effects on minor bulk trades should not be underestimated. The chart above illustrates this point, showing the percentages of regional minor bulk exports that are physically shut in because of the de facto closure of the Strait of Hormuz as well as the percentage of supplies at risk in the adjacent Gulf of Oman high-risk area. All numbers relate to the percentage affected of global seaborne volumes based on vessel tracking data in 2025. We note that this may not be 100% accurate due to the inherent challenges in classifying cargo type for some of the minor bulk trades.

In percentage terms, the most affected cargo is limestone, where 80% of global seaborne trade is seemingly at risk. Limestone has two primary uses: As the main raw material for clinker, i.e. the semifinished ingredient in cement (low quality, typically sourced domestically), and as a fluxing agent removing impurities in the molten iron in blast furnaces.

Seaborne limestone exports from the MEG is a very concentrated trade, principally from the UAE to India. While India has some domestic production of high-quality limestone grades required for blast furnaces, newer coastal steel mills are highly reliant on imports. Hence, if the MEG conflict and associated shut-in of limestone exports continues for several weeks, we may reach a point where Indian steel production has to be curtailed, secondarily affecting Indian iron ore and coking coal consumption.

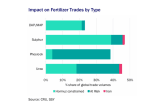

However, the most concerning impact of the current de facto Hormuz closure relates to the global seaborne fertilizer trade, of which approximately 20% is currently at risk, with most of that physically shut in.

This is concerning both with regards to the timing, with the Northern hemisphere planting season starting, and the importance of some of these volumes as feedstock in fertilizer production elsewhere in the world.

Sulphur, being a byproduct from MEG crude oil refining has both a production and a shipping problem, as the regional refinery utilization has dropped due to military attacks and a lack of distillate storage. Importantly, the ensuing loss of sulphur supply in the global market can quickly cascade into a drop into phosphate fertilizer (DAP/MAP) production elsewhere (e.g. Morocco), reducing the potential for substitution from the primary alternative suppliers. Phosphate rock supply is in a similar situation with, simultaneously, a large share of global export volumes shut in by the Hormuz closure, and processing elsewhere indirectly affected by the loss of sulphur (sulphuric acid). Urea exports from the MEG have been similarly shut in but, once again, there is a dual impact on the global fertilizer supply chain as exports of the feedstock ammonia have also been stopped. This then either increases the cost or curtails the production of MAP/DAP and urea elsewhere. All told, these indirect effects on global fertilizer supply are hard to assess quantitatively at the moment but are potentially of a similar order of magnitude as the direct shut-ins of exports in the MEG.

These critical supply side issues are compounded by the fact that the timing of the disruption occurs at the start of peak fertilizer application in the Northern hemisphere (March—May). South America is less vulnerable for now but would typically start forward buying in August/ September. Global commercial stocks of MAP/DAP are reportedly low, in part due to Chinese export controls since late 2024, with only India having meaningful government-directed stockpiles of DAP and urea for its immediate use. The impact on food production for the remainder of the year is a key worry, with expected lower grain yields in case the disruptions are prolonged.

By Roar Adland, Associate Partner & Global Head of Research

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business