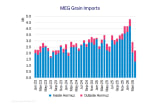

Countries in the Middle East Gulf (MEG) area have shown strong growth in agricultural imports in the past couple of years. According to vessel tracking data, agricultural imports totalled 38.6 Mt in 2025, an 18% increase from the prior 5-year average. Iran is the largest importer among the countries, at 15.2 Mt in 2025 according to vessel tracking data, half of which was corn. Iran was followed by Saudi Arabia (7.0 Mt in 2025), the UAE (4.8 Mt) and Iraq (5.8 Mt). The recent blockades of the Strait of Hormuz have disrupted inbound shipments to key grain discharge ports. If these countries are unable to find alternative routes, this would result in a loss of seaborne demand for grain and act as a negative for vessel demand. East Coast South America is a key supplier to the region, with Iran the second largest importer of Brazilian agricultural products, at 6% of the total in 2025.

For the countries in the region, imports make up a large proportion of domestic consumption, at 62% of corn, 65% of barley and 16% of wheat in 2024/25, USDA data show. While some of this can be partially met by increasing transits via overland routes or short sea, such as from Russia via the Caspian Sea, the region largely depends on the seaborne market, increasing the need to find routes via alternative ports.

Grain imports typically go to ports within the Strait of Hormuz, at 89% of seaborne imports in 2025. Since the outbreak of the US/Israel–Iran war at the end of February and the subsequent blockage of the Strait, shipments into the region fell dramatically. In March and April combined, the two months since the de facto closure, grain imports into the Strait dropped 75% year-on-year to 3.4 Mt. However, moderating the downside for dry vessel demand, shipments to the region outside of the Strait (Pakistan and some ports in Oman, the UAE and Iran) rose 64% in the same period to 1.7 Mt.

Specifically, shipments to Oman’s Sohar increased three-fold year-on-year to 0.5 Mt in March and April combined, while shipments to Fujairah were nearly doubled at 0.5 Mt. Similarly, shipments to the Iranian port of Chah Bahar rose from just one Panamax shipment in April and March last year to 0.5 Mt in the same period this year.

Following increased transits to the ports outside of the Strait, turnaround times for grain cargoes have increased. In the year to the end of February, before the war, the average turnaround time (the time between arrival and discharge) at the ports outside of Hormuz lifted from 9 to 16 days. Within this, the average time for grain discharging at Sohar doubled to 12 days. These ports often handle a range of bulk cargoes, which means that an increase in grain shipments puts pressure on the limited infrastructure available for grain handling.

Notably, shipments to Iran via the Strait have not ground to a halt despite the US blockade. In the three weeks since 13 April, the day on which the US started the blockade of any vessel calling at Iranian ports, grain arrivals have averaged 5 per week to Iran via the Strait, primarily shipments from Brazil. In the year to the week before the war, arrivals averaged around 8 per week. It is worth noting that due to the risks, vessels have been transiting the Strait with intermittent AIS broadcasting, which can disrupt vessel tracking data.

Without a clear end in sight to the Strait of Hormuz disruptions, an increase in shipments to ports in the region outside of the Strait has lessened the direct loss of volumes. While it is unclear currently how developed the overland infrastructure is from these ports to areas within the strait, the increase in shipments to these ports suggest they could be used as an alternative to the strait to mitigate food security concerns. Additionally, while still tentative, shipments have been continuing through the Strait and to Iran despite the US blockade.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business