Research

06/07/26

Aromatics Realignment: Benzene, Styrene and PX Trade Flows Reset the Q3 2026 Map for Chemical Tankers

The aromatics complex has spent the past three months adjusting to a structurally different trade map. Benzene, styrene and paraxy-lene are each reshuffling along distinct lines, but the common thread running through all three is the continued displacement of Mid-dle Eastern volumes following the closure of the Strait of Hormuz, layered onto a separate and partly unrelated story of European demand erosion and Asian capacity reshuffling. For the chemical tanker market, this matters less as a single shock and more as a redrawing of the corridors that earn freight — with some lanes losing density even as others gain tonne-miles.

Benzene: Europe Tightens, Asia Re-Routes

Europe’s prompt benzene market has moved into steep backwardation, a combination of buyers coming late to July purchasing after selling back June volumes, and unconfirmed heat-related production and logistics issues. Into that tightness, Indian benzene cargoes — increasingly unable to clear into the Middle East as Hormuz-related disruption persists — are finding a home in Europe and else-where in Asia. China’s benzene imports fell 47% month-on-month in May, driven almost entirely by a collapse in South Korean arri-vals rather than weak demand, with Middle Eastern and Indian cargoes only partially offsetting the shortfall.

Korean export data for the first 20 days of June illustrates the scale of the re-routing: of roughly 122,000 tonnes exported, around 113,000 tonnes went to China and only 9,000 tonnes to the US. The Europe-to-US benzene arbitrage that briefly opened in late May has also lost its underlying logic; with European prompt supply tight and backwardated, fresh westbound flows are unlikely without unusually strong US pull.

The structural picture into Q3 2026 is one of benzene staying largely trapped within Asia. India-to-China volumes strengthen as the historical India-to-Middle-East corridor (previously around 65% of India’s benzene exports) is impaired by Hormuz risk, Northeast Asian surplus continues to be absorbed regionally rather than pushed to the US given US tariffs and restored domestic TDP capacity, and Europe leans on China as an outlet for its own benzene length even as it imports prompt cargoes from India and the Middle East to cover near-term gaps.

Styrene: China Loses Share, Europe Becomes a Reluctant Importer

Styrene tells a different story. Europe’s benzene-styrene spread has inverted, compressing margins and pushing spot values down more than 40% from their April peak — the lowest since January — with run-rate cuts now being discussed for the second half. This is unambiguously a demand and margin problem rather than a supply one, and it means Europe is not, for now, a magnet for incremen-tal styrene imports from Asia or the US.

Within Asia, China is losing styrene export share to a recovering Northeast Asia. Japanese, South Korean and Taiwanese producers have secured naphtha from the Gulf of Mexico, North Sea and West Africa, allowing ethylene and benzene — and therefore styrene — output to recover just as Indian and South Korean buyers, traditionally large outlets for FOB China styrene, find more competitive alternatives. The practical effect is less China-to-India and China-to-Korea styrene flow, replaced by more intra-Northeast-Asia and Northeast-Asia-to-India trade.

The Q3 2026 picture is more consequential than the near-term one, however, because it is driven by the same Hormuz risk reshap-ing benzene. Kuwaiti and Saudi styrene exports to Europe and parts of Asia are exposed to continued Hormuz disruption, and Eu-rope’s rationalized, low-buffer styrene sector has little capacity to absorb a Middle Eastern shortfall on its own. The expected re-sponse is a structural pivot of European and some Asian styrene sourcing toward Asia (including China, once freight and war-risk premia are priced in) and North America, with Gulf Coast styrene increasingly flowing into Latin America and, at the margin, into Eu-rope. That implies a genuine long-haul demand build for Asia-to-Europe and US-to-Europe styrene cargoes through Q3, even as near-term China export activity remains cautious.

Paraxylene: The Structurally Tight Counterpoint

PX is the mirror image of benzene — tight rather than long — and the trade flow implications follow accordingly. China’s PX imports fell roughly a third month-on-month in May as feedstock disruption linked to the Middle East conflict cut operating rates outside China, though imports are expected to recover into June as those rates normalize. A cluster of Asian outages — Indonesia’s TPPI unit, Chi-na’s Fuhai Chuang plant, and a fire-delayed restart at Sinopec Yangzi — keeps Chinese import needs elevated into the second half.

The structural driver for Q3 2026 is India. With PX capacity growth across Asia lagging downstream PTA growth by a wide margin, and most of the new PTA capacity sited in India, GAIL’s new Mangalore PTA plant is expected to rely heavily on imported PX, pulling incre-mental volumes from the Middle East and wider Asia. Middle Eastern producers — well positioned to optimize between Turkey, India, the US and Asia — are likely to direct more tonnage toward India and, where tariff differentials favor it, the US, while Europe remains structurally long PX but increasingly constrained from shipping it to the US by the 15% tariff in place since August 2025, redirecting flows instead toward Mexico and Latin America.

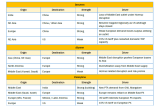

Q3 2026 Corridor Outlook

The tables below summarize the strongest expected corridors heading into Q3 2026 across the three aromatics streams.

What This Means for the Chemical Tanker Market

The freight implications of this aromatics reset run in two directions, and the net effect on Q3 2026 chemical tanker demand de-pends on which one dominates a given trade lane.

Benzene’s re-routing is, on balance, tonne-mile neutral to negative. The collapse in Northeast-Asia-to-China volumes is being re-placed by India-to-China and intra-Asia barrels, which largely substitutes one regional haul for another rather than adding net dis-tance or cargo density. Combined with the closure of the India-to-Middle-East corridor that previously absorbed roughly two-thirds of India’s benzene exports, the result is a benzene trade that is becoming more concentrated within Asia — supportive for fixture count, but not for the longer-haul employment that earns the best returns on chemical parcel tonnage.

Styrene points the other way. The structural pivot of European and Asian styrene sourcing toward Asia and North America, away from Middle Eastern barrels exposed to Hormuz risk, builds genuine long-haul Asia-Europe and US-Europe parcel demand — a trade that did not exist at this scale before the Middle East disruption began. This is the clearest source of incremental tonne-miles in the com-plex, and the one most likely to translate into firmer rates.

PX adds to that same long-haul build. The emerging Middle-East-to-India flow, tied to new PTA capacity at Mangalore, is a genuinely incremental corridor rather than a substitution for an existing one — GAIL’s reliance on imports in the absence of an OMPL restart creates demand that did not previously exist on this route. Like styrene, PX is a chemical cargo that moves on parcel tonnage, and a structurally tight PX balance across 2026 means this corridor should keep generating chemical tanker fixtures through Q3, with the added complication that the route itself carries Hormuz transit risk and the freight premia that come with it.

Taken together, the picture for Q3 2026 is one of bifurcated chemical tanker demand rather than uniform softness or strength. Ves-sels concentrated on short-haul intra-Asia and Asia-India distribution should see continued rate pressure as benzene volumes re-route along shorter regional paths and cargo density thins. Vessels with the flexibility and certification to swing onto the emerging long-haul styrene runs into Europe, or onto the Middle-East-to-India PX trade, should fare comparatively better, with Chinese and North American styrene exporters and Middle Eastern PX producers both positioned to see a genuine pickup in long-haul fixture activ-ity as the quarter progresses, assuming freight and war-risk premia settle at workable levels. The broader lesson is that Hormuz-driven trade disruption is not simply suppressing chemical tanker demand — it is redistributing it, rewarding owners who reposition tonnage toward the corridors gaining cargo at the expense of those still chasing volume on routes that are structurally thinning.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business