Q1 is typically a tough quarter for seaborne iron ore trade. Demand is disrupted by lunar new year holidays during which steel mills slow production, and supply is disrupted due to the wet season in north Brazil and the cyclone season in west Australia. Vessel tracking data show seaborne ore exports fell to 411 mt in Q1 2025, down 0.9% y-o-y. The main driver being a particularly bad cyclone season in west Australia.

The majority of the large miners have now published their production reports for the first quarter of the year and these reports provide some insight into the weather impact they have experienced, but also into what to expect for the rest of the year.

The Australian cyclone season, officially finished on 30th April, was the most active cyclone season since 2005- 06, with 25 tropical lows and 12 cyclones (8 of which were severe). Last year Australia experienced 13 lows, and 8 cyclones (6 of which were severe) over the same time period. Four storms in particular affected iron ore exports:

- Sean: 17th Jan – 22nd Jan

- Taliah: 31st Jan – 12th Feb

- Vince: 31st Jan – 4th Feb

- Zelia: 7th Feb – 15th Feb

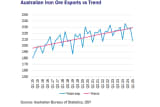

Little wonder then that Australian exports dropped to 207.9 Mt, the lowest quarterly export figure since Q1 2022. Nevertheless, all three major miners in Australia (Rio Tinto, BHP and Fortescue) have kept their guidance at the same levels for the rest of the year (BHP and Fortescue give guidance for the Australian financial year July-June, whilst Rio Tinto give guidance for the calendar year). This begs the question of whether we can expect a burst in activity in Q2 from pent up shipping demand from Q1?

Historical evidence suggests we can’t. Looking at historic export data for Australia since 2015 (the end of the period of rapid growth 2007-2014 when Australian exports grew at a compound annual growth rate of 15%), very poor Q1 exports don’t tend to be followed by particularly strong Q2 exports. Gauging the strength or weakness of each quarter by comparing it with a simple linear trend line there is very little negative correlation between Q1 and Q2.

The strongest Q2 in these terms at 16.8 Mt above trend, was in 2020 which followed a Q1 15.3 Mt below trend. The weakest Q1, 22.6 Mt below trend was in 2022, but was followed by a Q2 only 3.2 Mt above the trend line. Using the same trend Q1 of this year fell 21.2 Mt below the line.

The situation in Brazil was much less severe. Whilst Q1 exports were weak as usual (down 14.6% q-o-q), Vale, the main miner in the region, has taken measures to mitigate the impact of high rain levels over the last few years. Q1 exports from Brazil have increased every year since 2022. At 84.8 Mt this year’s figure is up 1.2% y-o-y. Vale have also retained their guidance for the rest of the year.

Based on the miners’ production reports there is no reason to expect that Q1 weakness should continue throughout the rest of the year. On the other hand, based on recent history there is also no reason to expect a surge in exports to offset the weakness. All things considered we expect some y-o-y growth in iron ore exports for the rest of the year from both Australia and Brazil.

By William Tooth, Senior Dry Bulk Analyst, Research, SSY.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business