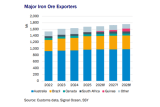

As we enter the new year, it is worth taking a moment to reflect on some of the developments that took place last year and what situation we are entering the new year in. Starting with by far the largest iron ore exporter, Australia has finished the year up 2.5% at 968.8 Mt. This included a very weak start to the year (-0.4% y-o-y in 1h25), which was subsequently reversed by strong growth in the second half of the year (+5% y-o-y). Predictably, average laden distances have remained stable, with China maintaining a share of 85% of shipments.

Interestingly, Brazil has continued to see a lessened impact of seasonality. Historically, there has often been a sharp drop in exports from December to those in January and February – partly due to the rainy season impacting the supply chain and partly due to maintenance scheduling ahead of subdued demand over Chinese New Year. However, since 2023 we have seen this seasonality reduced. In 1q23, Brazil’s exports declined 23% quarter-on-quarter; however, this dip lessened to 19% and 18% in 1q24 and 1q25, respectively. This, combined with a lift in fronthaul bauxite volumes, has reduced the typical weaker first quarter seasonality of Cape earnings.

One factor that counters this reduced volatility is the increasing market share of smaller iron ore producers in Brazil. Smaller producers shipments rose 10% y-o-y, driving Brazil’s 2% growth to 392 Mt in 2026 as Vale’s shipments declined 1%. As the chart below demonstrates, Vale exports show both lower quarterly volatility than the minor miners and slightly reduced quarterly volatility over time. However, Vale of course still accounts for the bulk of Brazilian shipments. December 2025 marked the first shipment from Guinea’s Simandou iron ore project on the 203k dwt Winning Youth.

With the turnaround time for this first shipment out of Morebaya port lasting close to a month, Guinean iron ore exports in 2025 got off to a slower start than expected. However, the second shipment, also in December, had a shorter turnaround time of 5 days and is presumably more indicative of conditions going forward.

West Africa’s seasonality is likely to play a less influential role on iron ore shipments this year than has been the case for bauxite exports. Typically, shipments from the country slow down during June–October due to the rainy season. However, as the Simandou project is in its ramp[1]up phase to maximum capacity, rail constraints appear to be playing a more important role. Rio Tinto has published its 2026 guidance for Simandou at 5-10 Mt. With WSC share the same size, the range for overall exports appears to be projected at 10-20 Mt for 2026.

In the North Atlantic, Canadian iron ore returned 2% year -on-year growth last year at 65.6 Mt. The first half of the year rose 4%, while the second half lifted 1%. Meanwhile, shipments from Narvik, Norway, rose 20% on the year to 21.7 Mt, after a train derailment curbed exports in 2024.

Elsewhere, some smaller producers have seen a decline in shipments. Exports from Peru declined (-15% to 19.4 Mt) in 2025 as exports were hindered by port infrastructure issues mid-year. Meanwhile, as competitive producers in the South Atlantic ramp up, higher-cost producer’s exports have been put under pressure. As a result, Indian and Ukrainian exports fell 26% and 15% to a respective 29.2 Mt and 12.5 Mt.

The pace of Guinea’s iron ore ramp-up will continue to be a focal point through 2026, as its high-quality and lower[1]cost iron ore puts pressure on other producers. We thus expect to see a continuation of these export trends in the new year.

Cara Hatton, Dry Bulk Senior Analyst, Research, SSY

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business