As iron ore prices edge lower and the market tilts into surplus, grade is no longer a marginal pricing variable, it is becoming the dividing line between commercially viable tonnes and stranded supply. For market participants, the next two years may not simply be about price direction, but about which tonnes move, from where, and at what realised margin.

Benchmark prices are expected to soften from ~$100/t toward the low-$90s as new supply meets structurally weaker Chinese steel demand. Seaborne iron ore trade stood at roughly 1.7 Bt in 2025, with China importing around 1.3 Bt. Against this backdrop, the ramp-up of high-grade African tonnes, led by Simandou, marks a pricing and freight inflection point. Simandou is expected to deliver 120 Mt by 2030, around 10% of China’s seaborne import demand. A single high-grade, low-cost project averaging mid-to-high 60% Fe could displace a meaningful share of marginal tonnes globally, making spreads, rather than flat prices, the primary trading lever.

Grade differentials are crucial, especially as prices drop and mills become selective. Higher-grade ore (65-68% Fe) boosts blast furnace efficiency, lowers coke use, and cuts emissions, critical factors given decarbonisation targets and Europe’s CBAM. Historically, the 65-62% spread widens during downturns, with a $10–15/t premium potentially decisive in a $90/t market. However, the system has a limit to how much high-grade ore it can absorb at high premiums, as mills blend grades to meet furnace specifications. Excessive high-grade supply in a weak market can narrow premiums. In an efficient market, pricing adjusts so buyers are broadly indifferent at the margin between grades once blending and productivity gains are factored in. Even so, higher-grade units tend to retain value where emissions and fuel efficiency matter.

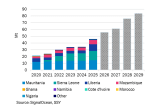

Africa’s emerging supply profile amplifies this shift. Beyond Simandou, notable projects in Guinea, Gabon, Liberia and Sierra Leone could conservatively inject ~20–30 Mt of seaborne supply by 2028, and are crucially backed by Chinese investors. Much of this material sits high on the grade curve and low on the cost curve (around $30-35/t FOB), pressuring mid-grade and higher-cost producers in a declining price environment.

Australia remains cost competitive, but its average export grade has gradually declined, prompting benchmarks to shift from 62% toward 61% Fe. If Chinese buyers substitute even 50-80 Mt of Australian mid-grade cargoes with West African high-grade material, tonnemile demand reshapes. Guinea-China voyages are significantly longer than Australian routes, supporting Capesize demand even if headline volumes remain flat. Brazil is less vulnerable, with Carajás entrenched in long-term supply chains. Displacement risk instead sits with smaller producers. India’s lower-grade exports are declining as domestic steel demand absorbs supply, potentially turning the country into a net importer of high-grade material. High-cost Canadian and European mines may increasingly serve captive operations.

For Panamax and Capesize markets, Africa’s expansion and potential US and Europe-bound flows introduce optionality. If European mills increase imports of African high-grade ore to comply with emissions standards, some Atlantic basin trade patterns could reconfigure, potentially displacing shorter-haul Canadian shipments and modestly extending tonne-miles.

The broader conclusion is clear: the next cycle rewards optionality in grade and geography. While headlines focus on flat prices, profitability will depend on grade spreads and delivery terms. African supply growth is not merely incremental volume; it represents a structural re-routing of flows. In a surplus market, low-grade tonnes risk not moving at all.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business