Though steel export volumes are not significantly impacted by the closure of Hormuz, it would directly impact EAF production through higher energy prices. While almost 90% of BOF-based (basic oxygen furnace) steel production is dependent on coking coal prices, the EAF-based (electric arc furnace) production is particularly exposed with 50% of the energy input relying on electricity and 38% on natural gas.

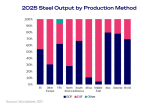

Even before this war, without subsidies, EAF-based steelmaking was often more costly than BF–BOF. With energy making up 15–20% of EAF costs, higher gas and power prices would put EAF-based production at a much bigger disadvantage. Though only 30% of global steel output is through EAF, certain regions of the world are a lot more exposed. While only 19% of Asian steelmaking is EAF based, North America, Europe and Africa are more exposed with 72%, 52% and 89% of production, respectively, being EAF-based, based on 2025 figures.

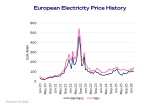

The damage from high energy prices was already evident in Europe in 2H22, when the region idled more than 30 Mt of steel capacity after power prices surged following the Russo-Ukrainian war. With electricity prices remaining high, EAF margins never fully recovered, and many idled mills never restarted. With steelmakers also under pressure from the EU ETS, another energy shock could trigger further closures. This time around, despite stronger renewable generation since 2022, major producers such as Germany and Italy remain exposed. Even if Hormuz re-opens soon, the damage done to the Gulf energy infrastructure appears to be long-lasting.

Elsewhere, the impact is more contained. The US is also EAF-dominant, but abundant domestic gas supply and disconnected pricing protect it from global gas shocks. In Africa, countries such as Egypt and Algeria are likely to see a notable squeeze in margins, but with the continent accounting for only around 5% of global steel production, the broader market impact should remain limited.

In Asia, India is especially exposed to current events, more than any other country. It employs a significant EAF fleet of ~60% of annual production, and being one of the major importers of MEG oil and gas volumes its steel sector remains under significant threat. Its BOF steel is even more exposed than EAF as it is very dependent on imported limestone from the UAE as a fluxing agent in the steelmaking process. With both EAF and BOF affected by the Hormuz closure, Indian steel production will be significantly impacted by the ongoing war.

China’s relatively well insulated thanks to its large BOF base (~90%), and could be the answer any Indian steel shortages. Some of its BOF surplus capacity will likely be used to replace weaker EAF production, but with enough seaborne demand that excess capacity could easily be redirected to international markets.

Japan and Korea’s BOF fleet are also set to benefit from rising EAF production costs. Both have sizeable BOF fleets and plenty of spare capacity to lift production if energy prices stay elevated. Though, like China, some of that slack will be used to replace weaker domestic volumes from their EAF fleet, it could also be directed to the international markets.

Although steel production in the Far East and the US seems relatively insulated compared with other regions, it remains uncertain whether this will translate into higher export volumes, as a weakened macroeconomic outlook could suppress global steel demand. At first glance, Asia’s large BOF steelmaking capacity appears to shield the market from rising energy costs. In reality, much of this surplus capacity will likely be deployed to offset reduced EAF output and stabilise domestic prices. Limestone supply disruptions further limit the region’s flexibility as India’s both EAF and BOF-based steelmaking are significantly exposed to the closure of Hormuz.

Articles

You may also be

interested in

View all

Get in touch

Contact us today to find out how our expert team can support your business